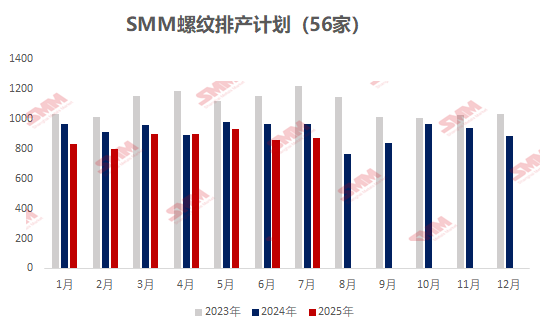

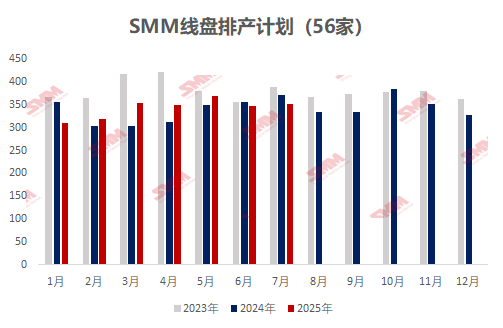

Since April 2022, the SMM rebar production schedule sample has been expanded to include 56 enterprises.

According to the SMM survey data from 56 key steel-producing enterprises:

- The planned rebar production for July was 8.6913 million mt, an increase of 91,600 mt from the actual production in June, representing a growth rate of 1.07%.

- The planned wire rod production for July was 3.5198 million mt, an increase of 38,900 mt from the actual production in June, representing a growth rate of 1.12%.

Chart-1: Rebar & Wire Rod Production Schedule of Mainstream Construction Steel Mills (56 Enterprises)

Data Source: SMM

Overall:

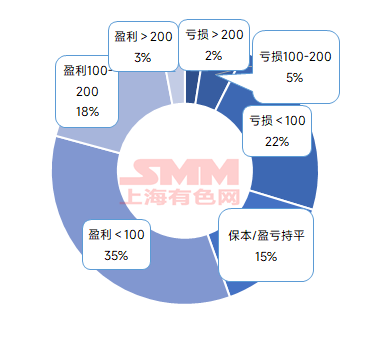

In June, the national construction steel prices bottomed out and rebounded. During the first and second ten-day periods of the month, there was a macro vacuum period in China. In the third ten-day period, the Central Financial and Economic Affairs Commission meeting issued signals on addressing cut-throat competition, coupled with the news of production restrictions at steel mills in the southwest region, which boosted market sentiment and led to a bottom-up rebound in spot prices. On the cost side, the price trends of raw materials and finished products were similar, and steel mill profits showed little change compared to June, with overall benefits continuing to range between (-200-200). In July, the total production of construction steel materials at steel mills increased slightly, but the daily rebar production decreased by 2.2% MoM, and the daily wire rod production decreased by 2.14% MoM. Most steel mills maintained their previous production levels, but some individual manufacturers had better order-taking for specialty steel products and stronger profit performance than rebar, leading to a slight shift of pig iron towards specialty steel products. Specifically, the planned construction steel production in the central-south and north-west regions increased. On the one hand, steel mill profits from producing construction steel materials were moderate. On the other hand, some manufacturers upgraded their hot-rolled coil production lines, redirecting surplus pig iron towards construction steel materials. In contrast, some steel mills in the east China region shifted towards producing medium-thickness plates, high-quality wire rods, and other varieties. Some individual steel mills had outstanding steel billet orders from earlier periods that had not yet been fully delivered, leading to a continued reduction in construction steel production.

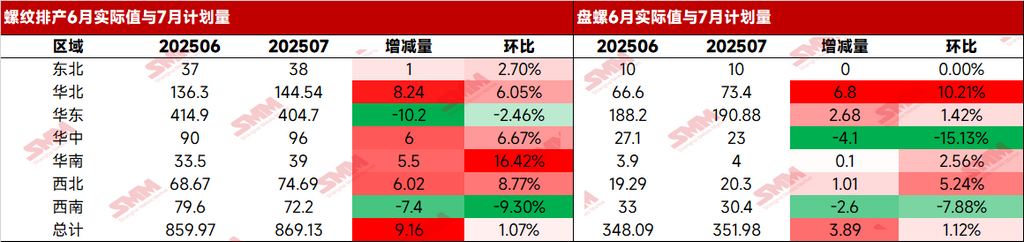

By region:

Table 1: Actual Rebar and Coiled Rebar Production in June vs. Planned Production in July

Data Source: SMM

In the northeast region, steel mill profits ranged between (-100-200), and manufacturers maintained normal production levels. Some individual steel mills continued to focus on producing specialty steel products, resulting in little change in construction steel production in recent months.

In the north China region, steel mill profits ranged between (-250-200), with significant differentiation among steel mills. Currently, steel mills that are profitable in producing construction steel materials have increased their rebar and wire rod production in July. However, considering that some manufacturers have specialty steel product lines, they prioritize ensuring the production of specialty steel products while limiting the amount of pig iron redirected to construction steel materials. Therefore, the overall increase in construction steel production in July is limited.

In the east China region, steel mill profits ranged between (0-300). Currently, steel mills in this region have better profitability in producing construction steel materials compared to other regions. Most steel mills maintain their previous production status, but some individual manufacturers in Jiangsu have received steel billet orders until the end of September and will continue to reduce their construction steel production in July. In Shandong and Fujian, some individual steel mills have redirected part of their pig iron to specialty steel products, resulting in a slight decrease in rebar production and a 2.46% decrease in rebar production in the region in July.

In north-west China, steel mill profits range from (-200 to 50). Recently, the profitability of steel mills has changed relatively little. Steel mills that underwent maintenance earlier have not yet resumed production. However, some steel mills have plans to renovate their coil rolling lines in July, redirecting pig iron to rebar production, resulting in a slight increase in daily output.

In central and south China, steel mill profits range from (-100 to 150). Some steel mills have resumed production of bars and wires. In July, rebar production returned to normal levels, with a 9.31% MoM increase. Some manufacturers have good orders for industrial wires, so they have reduced wire rod production and increased industrial wire production.

In south-west China, steel mill profits range from (-200 to 100). Multiple steel mills in Yunnan are already operating at a loss. Coupled with significant pressure on in-plant inventory, production in July decreased significantly. Additionally, BF and EAF steel mills in Guizhou have arranged maintenance and production suspension plans, limiting the production of construction materials. Steel mills in Sichuan and Chongqing are basically producing according to plan.

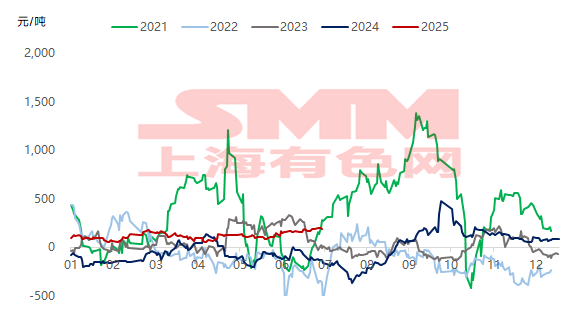

Chart-2: Trend of real-time profits for rebar production by steel mills from 2021 to the present

Data source: SMM

Chart-3: Marginal profit situation for rebar production by sample steel mills at the beginning of July

Data source: SMM

Looking ahead,steel mill production will continue to be profit-driven. As most manufacturers earn profits from producing construction materials, their short-term production enthusiasm remains high. However, some manufacturers producing multiple varieties will prioritize high-profit varieties. Coupled with the slowdown in market and downstream digestion during the off-season, some regions face significant pressure on in-plant inventory, limiting the upward potential for increased construction material production. This has led to a decrease in the daily average production of construction materials by steel mills in July. Although the profitability of EAF steel mills has improved, most are still operating at a loss, and it is expected that there will be no significant increase in short-term production. On the demand side, high temperatures and frequent rainfall are prevalent in July and August, limiting the construction progress of site projects. During the seasonal off-season for demand, overall transactions are unlikely to see significant improvement.Overall, steel mills currently have considerable profit margins, and it is unlikely that there will be significant production cuts in the short term. However, considering the pressure of inventory accumulation during the off-season, some manufacturers still plan to adjust their product mix. There is an expectation of a decrease in construction material production in the medium and long term.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)